When Good News is Bad News: A Hot Labor Market Collides With Your Mortgage Rate

There's an old trader's joke that the economy is the only place where "good news" can send everyone running for the exits. This week, that joke is doing some heavy lifting.

The jobs data just came in hot—genuinely hot, the strongest stretch we've seen in well over a year. And yet anyone hoping for lower mortgage rates this summer should be reading those headlines with one eye closed. Here's why the picture is more complicated than the cheerful numbers suggest, and what it means if you're trying to buy, sell, or simply make sense of where housing goes from here.

The labor market woke up

Start with the job openings. The latest JOLTS report (that's Job Openings and Labor Turnover, the government's monthly read on how many roles employers are trying to fill) showed openings leaping roughly 11% in a single month, climbing to 7.6 million. Wall Street wasn't expecting anything close to that. It was the kind of beat that makes economists do a double-take.

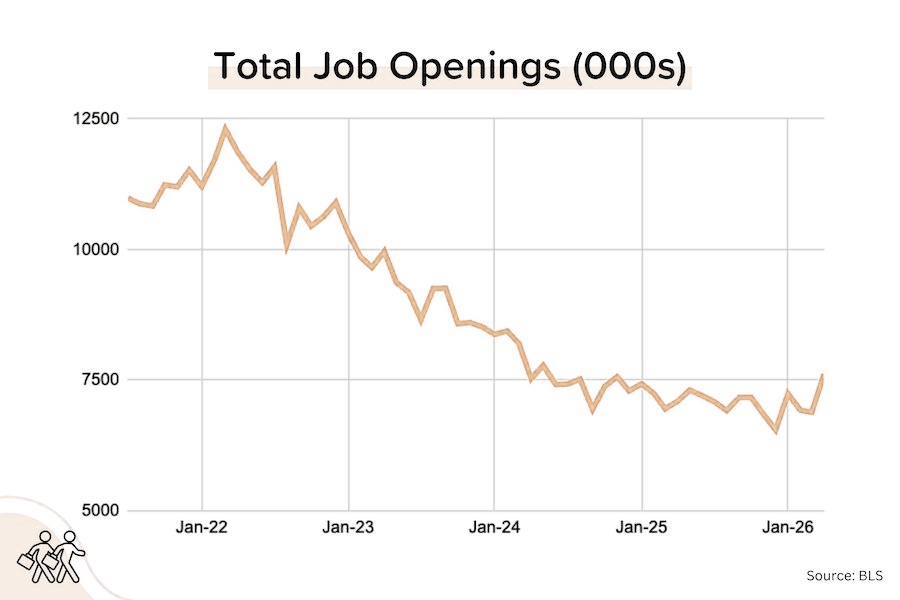

Figure 1: The Long View

Total Job Openings, in thousands

Openings peaked near 12.3 million in early 2022 and ground steadily lower for almost two years before flattening around 7.5 million. The latest uptick to roughly 7.6 million is the first real move higher in a while — hence the bottoming debate. Source: BLS.

But here's the asterisk worth pausing on: almost the entire jump—about 91% of it—came from one corner of the economy, Professional and Business Services. That category alone rocketed to its highest level of openings in roughly two years. When a single sector accounts for nearly all of a "broad" improvement, it's fair to wonder whether we're watching a genuine turning point or a statistical quirk that'll get revised away next month. Maybe openings have finally found a floor. Maybe the data is just noisy. We'll need another month or two to know.

Then came the private payroll picture. ADP, which tracks hiring at private companies, reported about 122,000 jobs added in May—the best monthly showing since the start of 2025. Wages stayed sturdy too: people who kept their jobs saw pay rise around 4.4% over the year, while those who switched employers pocketed closer to 6.5%. Neither figure has moved much in nine months, which tells you the labor market has been quietly resilient rather than dramatically reheating.

So what do we make of it? Either the underlying economy is tougher than the soft GDP print (first-quarter growth limped in around 1.6% annualized) would suggest—or the AI boom that was supposed to be vaporizing jobs is, at least for now, creating more than it destroys. Both stories are plausible. Both are worth watching.

Why strong jobs can mean stubborn rates

Now for the part that stings. A roaring labor market is exactly the kind of thing that keeps the Federal Reserve cautious—and right now, "cautious" is leaning in an uncomfortable direction.

The Fed's policy rate currently sits at 3.50–3.75%. A few weeks ago, the market treated additional cuts or a long hold as the obvious path. That confidence is fraying. Futures pricing now shows the odds of the Fed simply holding rates steady slipping at each upcoming meeting—not because cuts are coming, but because the probability of an outright hike is creeping higher.

A year ago the question was how many times the Fed would cut. Today it's whether they'll be forced to raise.

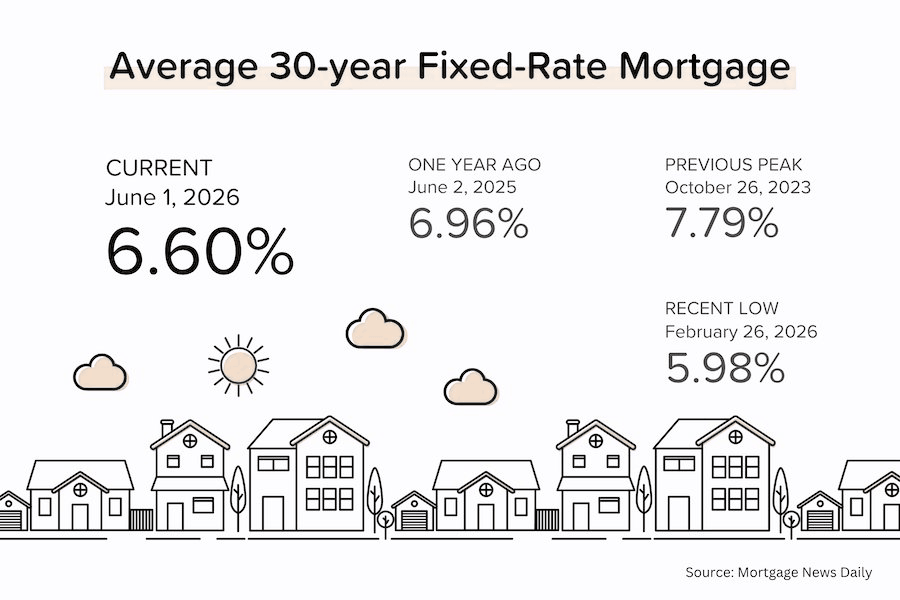

Figure 2: Where Rates Stand

Average 30-year fixed-rate mortgage

The 30-year fixed sits near 6.60% — down from 6.96% a year ago and far below the October 2023 peak of 7.79%, but back up from a February low of 5.98%. Source: Mortgage News Daily.

The meeting calendar tells the story. June's gathering—the first chaired by the newly installed Kevin Warsh—still looks like a near-certain hold. But look further out and the cracks widen: by late summer the market is penciling in a small but rising chance of higher rates, and by the Fed's final meeting of the year in December, traders now see better-than-even odds that rates end 2026 above where they started. A year ago, the conversation was about how many times the Fed would cut. Today it's about whether they'll be forced to raise.

What changed? Largely the oil market. We have a ceasefire that gets violated daily and a "peace deal" shadowed by threats to choke off the Strait of Hormuz entirely. In that fog, the bond market is bracing for oil-driven inflation to linger. And when bond investors brace for inflation, they demand higher yields—which feeds almost directly into the mortgage rates you and I pay. Strong jobs plus jittery oil is not the cocktail that produces a refi wave.

Housing: flat headline, restless undercurrent

If you only read the national home-price number, you'd assume the market had fallen asleep. Cotality's data shows prices up a barely-there 0.3% over the past year.

And yet the same firm just raised its forecast for annual price growth to about 5.3%. On a median home around $417,500, that's roughly $23,000 in appreciation—real money. The disconnect is the interesting part. Their chief economist makes the case that the "national market" is largely a fiction: beneath that flat average, certain metros—especially job-rich pockets of the West and more affordable Midwest markets—are quietly accelerating while others sag. The average cancels them out. Read the local story, not the national one.

So what justifies the optimism on price growth? They don't spell it out, but the math only works if you assume mortgage rates ease meaningfully by year-end—something in the high-5% to 6% range on the 30-year fixed. Given everything we just covered about the Fed and oil, that's an aggressive bet. Worth keeping in mind before you treat any forecast as gospel.

Buffett's company places its chips on housing

Here's the move that should make everyone sit up. Berkshire Hathaway just agreed to buy homebuilder Taylor Morrison in an all-cash deal worth around $7 billion—a 24% premium to the prior closing price, and the first acquisition under Berkshire's new CEO, Greg Abel.

The valuation is the tell. Berkshire is paying roughly one times revenue, nine times earnings, and a hair below book value. Those are bargain-bin multiples—exactly what you'd pay if you believed a cyclical upturn in housing is coming and wanted to buy before the rest of the market figures it out. Taylor Morrison leans into Sun Belt growth markets like Florida, Texas, and Arizona, and courts move-up and lifestyle buyers (think resort-style communities) rather than living or dying by first-time-buyer demand. Abel has signaled the plan is to fold Taylor Morrison into Berkshire's already-enormous footprint across the housing ecosystem over time. When the most patient money in America quietly buys a homebuilder on the cheap, it's at least worth asking what they see that the headlines don't.

The hidden tax keeping America stuck in place

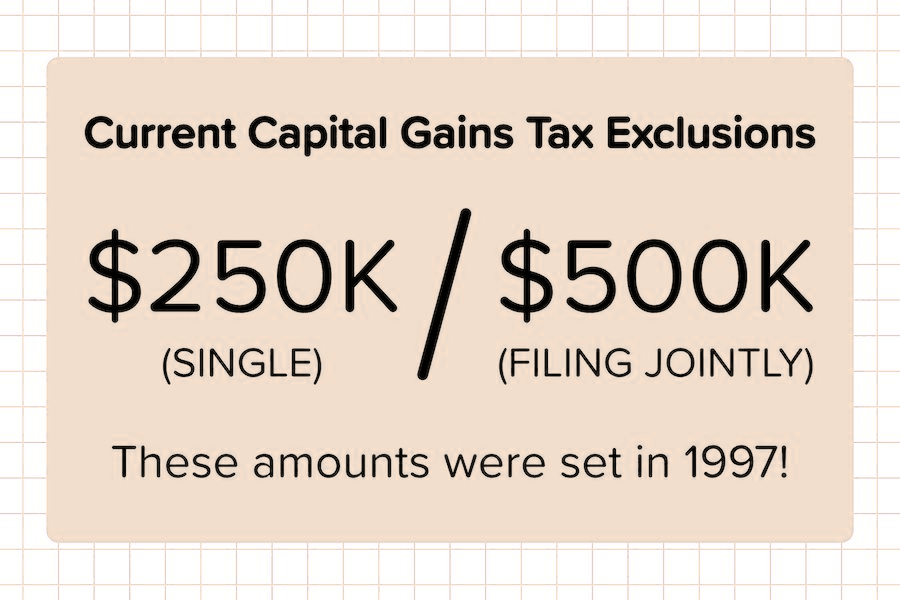

One last piece of the puzzle, and it explains a lot about why inventory stays so tight. When you sell your primary home, you can shield a chunk of the gain from capital gains tax—$250,000 if you file single, $500,000 if you file jointly.

Stuck at $250K (single) / $500K (joint) since 1997 — while home prices have roughly tripled-and-a-half.

Those numbers sound generous until you notice the date they were set: 1997. Home prices have roughly tripled-and-a-half since then, but the exclusion hasn't budged an inch. The result, per the National Association of Realtors, is that more than 25 million homeowners are now sitting on gains above $250,000, and over 8 million are past the $500,000 line. For all of them, selling means writing the IRS a sizable check—yet another reason to simply stay put.

There are proposals floating around Congress to fix this (one would double the exclusions), but they're crawling rather than sprinting. Until something changes, this quiet tax math is one more force locking owners into homes they might otherwise list.

The bottom line

We're in a strange moment where the economy keeps flashing strength, and that strength is precisely what's threatening to keep borrowing costs high. Housing looks frozen on the surface while serious money bets on a thaw underneath. And a 30-year-old tax rule keeps millions of would-be sellers glued in place.

If there's a single takeaway, it's this: stop reading the national averages as your personal forecast. Rates, prices, and opportunity all live at the local level right now—and the gap between the headline and your neighborhood has rarely mattered more.

This post is for general information and isn't financial, tax, or investment advice. Talk to a qualified professional about your specific situation before making a move.